14. Correlation and Regression

14.10 Multiple Regression

Multiple regression is to the linear regression we just covered as one-way ANOVA is to  -way ANOVA. In -way ANOVA we have one DV and discrete IVs. With multiple regression we have one DV (univariate) and

-way ANOVA. In -way ANOVA we have one DV and discrete IVs. With multiple regression we have one DV (univariate) and  continuous IVs. We will label the DV with

continuous IVs. We will label the DV with  and the IVs with

and the IVs with  . The idea is to predict with

. The idea is to predict with  via

via

![\[y^{\prime} = a + b_{1} x_{1} + b_{2} x_{2} + \cdots + b_{k} x_{k}\]](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-00076fd4ffbb4a156277abef24b695e7_l3.png "Rendered by QuickLaTeX.com")

or, using summation notation

![\[y^{\prime} = a +\sum_{j=1}^{k} b_{j} x_{j}\]](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-daa390f4ab9c3b09b566dec79f30b537_l3.png "Rendered by QuickLaTeX.com")

Sometimes we (and SPSS) write  . The explicit formula for the coefficients

. The explicit formula for the coefficients  and

and  are long so we won’t give them here but, instead, we will rely on SPSS to compute the coefficients for us. Just the same, we should remember that the coefficients are computed using the least squares method, where the sum of the squared deviations is minimized. That is, and the are such that

are long so we won’t give them here but, instead, we will rely on SPSS to compute the coefficients for us. Just the same, we should remember that the coefficients are computed using the least squares method, where the sum of the squared deviations is minimized. That is, and the are such that

![\begin{eqnarray*} E & = & \sum_{i=1}^{n} (y_{i} - y^{\prime}_{i})^{2} \\ & = & \sum_{i=1}^{n} (y_{i} - [a + \sum_{j=1}^{k} b_{j} x_{ji}])^{2} \end{eqnarray*}](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-44a599f8b3cd6a1036292d98ab8ef336_l3.png "Rendered by QuickLaTeX.com")

is minimized. (Here we are using  to represent data point

to represent data point  .) If you like calculus and have a few minutes to spare, the equations for and the can be found by solving:

.) If you like calculus and have a few minutes to spare, the equations for and the can be found by solving:

![\[ \frac{\partial E}{\partial a} = 0, \;\;\; \frac{\partial E}{\partial b_{1}} = 0, \;\;\; \cdots \;\;\; \frac{\partial E}{\partial b_{k}} = 0 \]](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-0132cf5868a938bddef3c5ee1d326123_l3.png "Rendered by QuickLaTeX.com")

for and the . The result will contain al the familiar terms like  ,

,  , etc. It also turns out that the “normal equations” for and the that result have a pattern that can be captured with a simple linear algebra equation that we will see in Chapter 17.

, etc. It also turns out that the “normal equations” for and the that result have a pattern that can be captured with a simple linear algebra equation that we will see in Chapter 17.

Some terminology: the (including  ) are known as partial regression coefficients.

) are known as partial regression coefficients.

14.10.1: Multiple regression coefficient, r

An overall correlation coefficient,  , can be computed using pairwise bivariate correlation coefficients as defined in the previous Section 14.2. This overall correlation is defined as

, can be computed using pairwise bivariate correlation coefficients as defined in the previous Section 14.2. This overall correlation is defined as  , the bivariate correlation coefficient of the predicted values versus the data . For the case of 2 IVs, the formula is

, the bivariate correlation coefficient of the predicted values versus the data . For the case of 2 IVs, the formula is

![\[ r = \sqrt{\frac{r_{y x_{1}}^{2} + r^{2}_{y x_{2}} - 2 r_{y x_{1}} r_{y x_{2}} r_{x_{1} x_{2}} }{1 - r^{2}_{x_{1} x_{2}}}} \]](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-e99c7d03ecfd4705430b96106ca5be0d_l3.png "Rendered by QuickLaTeX.com")

where  is the bivariate correlation coefficient between and

is the bivariate correlation coefficient between and  , etc. It is true that

, etc. It is true that  as with the bivariate .

as with the bivariate .

Example 14.6 : Suppose that you have used SPSS to obtain the regression equation

![\[ y^{\prime} = -44.572 + 87.679 x_{1} + 14.519 x_{2} \]](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-af8db193c6daef2eabae54be9845469b_l3.png "Rendered by QuickLaTeX.com")

for the following data :

| Student | GPA, |

Age, |

Score, |

|

|

|

|

|

|

| A | 3.2 | 22 | 550 | 10.24 | 484 | 302500 | 1760 | 12100 | 70.4 |

| B | 2.7 | 27 | 570 | 7.29 | 729 | 324900 | 1539 | 15390 | 72.9 |

| C | 2.5 | 24 | 525 | 6.25 | 576 | 275625 | 1312.5 | 12600 | 60 |

| D | 3.4 | 28 | 670 | 11.56 | 784 | 448900 | 2278 | 18760 | 95.2 |

| E | 2.2 | 23 | 490 | 4.84 | 529 | 240100 | 1078 | 11270 | 50.6 |

|

|

|

|

|

|

|

|

|

|

Compute the multiple correlation coefficient.

Solution :

First we need to compute the pairwise correlations  ,

,  , and

, and  . (Note that =

. (Note that =  , etc. because the correlation matrix is symmetric.)

, etc. because the correlation matrix is symmetric.)

![\begin{eqnarray*} r_{x_{1}y} & = & \frac{n(\sum x_{1} y) - (\sum x_{1} ) (\sum y )}{\sqrt{[n (\sum x_{1}^{2}) - (\sum x_{1})^{2}] [n (\sum y^{2}) - (\sum y)^{2}}]}\\ & = & \frac{5(7967.5) - (14 ) (2805 )}{\sqrt{[5 (40.18) - (14)^{2}] [5 (1592025) - (2805)^{2}}]}\\ & = & 0.845 \end{eqnarray*}](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-f2bbe656e45f87cb2d868e539d669f27_l3.png "Rendered by QuickLaTeX.com")

![\begin{eqnarray*} r_{x_{2}y} & = & \frac{n(\sum x_{2} y) - (\sum x_{2} ) (\sum y )}{\sqrt{[n (\sum x_{2}^{2}) - (\sum x_{2})^{2}] [n (\sum y^{2}) - (\sum y)^{2}}]}\\ & = & \frac{5(70120) - (124 ) (2805 )}{\sqrt{[5 (3102) - (124)^{2}] [5 (1592025) - (2805)^{2}}]}\\ & = & 0.791 \end{eqnarray*}](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-d3e738b287071b2a040aa4a2ef63edef_l3.png "Rendered by QuickLaTeX.com")

![\begin{eqnarray*} r_{x_{1}x_{2}} & = & \frac{n(\sum x_{1} x_{2}) - (\sum x_{1} ) (\sum x_{2} )}{\sqrt{[n (\sum x_{1}^{2}) - (\sum x_{1})^{2}] [n (\sum x_{2}^{2}) - (\sum x_{2})^{2}}]}\\ & = & \frac{5(349.1) - (14 ) (124)}{\sqrt{[5 (40.18) - (14)^{2}] [5 (3102) - (124)^{2}}]}\\ & = & 0.371 \end{eqnarray*}](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-075ef194a2122b3250bab3c85fcf4c0d_l3.png "Rendered by QuickLaTeX.com")

Now use these in :

▢

14.10.2: Significance of r

Here we want to test the hypotheses :

where  is the population multiple regression correlation coefficient.

is the population multiple regression correlation coefficient.

To test the hypothesis we use

![\[ F_{\mbox{test}} = \frac{r^{2} / k}{(1-r^{2})/(n-k-1)} \]](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-0865fcb5f2faf146add3a337ce13819f_l3.png "Rendered by QuickLaTeX.com")

with

![\[ \nu_{1} = n-k \mbox{\ \ \ (d.f.N.)\ \ \ \ and\ \ \ \ } \nu_{2} = n-k-1 \mbox{\ \ \ (d.f.D.)} \]](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-7cfecfae923aaa41db8edf8f17635309_l3.png "Rendered by QuickLaTeX.com")

here:

(Note: This “ -test” is similar to but not the same as the “ANOVA” output given by SPSS when you run a regression.)

-test” is similar to but not the same as the “ANOVA” output given by SPSS when you run a regression.)

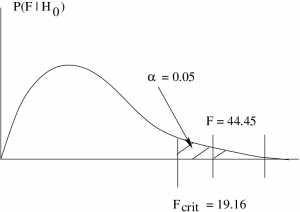

Example 14.7 : Continuing with Example 14.6, test the significance of .

Solution :

1. Hypotheses.

2. Critical statistic. From the Rank Correlation Coefficient Critical Values Table (i.e., the critical values for the Spearman correlation) with

find

![\[ F_{\mbox{crit}} = 19.16 \]](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-412ac5646fcc8414ef6f67d1c85600ff_l3.png "Rendered by QuickLaTeX.com")

3. Test statistic.

4. Decision.

Reject  .

.

5. Interpretation.

is significant.

is significant.

▢

14.10.3: Other descriptions of correlation

- Coefficient of multiple determination:

. This quantity still has the interpretation as fraction of variance explained by the (multiple regression) model.

. This quantity still has the interpretation as fraction of variance explained by the (multiple regression) model. - Adjusted :

![\[ r^{2}_{\mbox{adj}} = 1 -\ \left[ \frac{(1-r^{2})(n-1)}{n-k-1} \right] \]](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-1c123c03b06f050825ce7a3346d5ed40_l3.png "Rendered by QuickLaTeX.com")

gives a better (unbiased) estimate of the population value for

gives a better (unbiased) estimate of the population value for  by correcting for degrees of freedom just as the sample

by correcting for degrees of freedom just as the sample  with its degrees of freedom equal to

with its degrees of freedom equal to  gives an unbiased estimate of the population

gives an unbiased estimate of the population  .

.

Example 14.8 : Continuing Example 14.6, we had so

![\[ r^{2} = 0.978 \]](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-43a1d4d02904d0438a888d1faafa24f5_l3.png "Rendered by QuickLaTeX.com")

and

![\begin{eqnarray*} r^{2}_{\mbox{adj}} & = & 1 -\ \left[ \frac{(1-r^{2})(n-1)}{n-k-1} \right] \\ r^{2}_{\mbox{adj}} & = & 1 -\ \left[ \frac{(1-0.978)(5-1)}{5-2-1} \right] \\ & = & 0.956 \end{eqnarray*}](https://openpress.usask.ca/app/uploads/quicklatex/quicklatex.com-b5d5ada7832af5e06c37dcd98e0299d0_l3.png "Rendered by QuickLaTeX.com")

▢