6.2 Life Cycle Costs

In the Evaluation Methods chapter, we discussed many methods which an investor might use to choose between mutually exclusive projects. The drawback of many of these methods is that they do not account for every economic factor which might impact a project. For example, the Capital Recovery Cost (CRC) method considered the initial price and final salvage value of a project, but did not consider other cash flows such as maintenance costs or revenues. The purpose of life cycle costing is to look at all of the costs related to a project, so that its cost-effectiveness can be evaluated with greater confidence.

Life cycle cost (LCC) is the total cost of a project over its life including planning, design, acquisition, support costs, and decommissioning, as well as any other costs directly attributable to owning or using the asset. These costs encompass the entire life cycle of a project and thus are sometimes referred to as “cradle to grave” costs. They are typically measured or estimated in advance, however, life cycle costing can be applied at any phase of a project’s life. It can provide insight into how the manufacturing, installation, operation, maintenance, or disposal of an existing project can be executed economically. The major advantages of performing life cycle costing at the outset are that cost-effective decisions will have a greater influence on the total cost of a project if they are enacted early, and identifying project costs in advance allows an investor to account for their preferences (performance, reliability, maintenance, etc.) before beginning a project.

When estimating the LCC of a project, we break down the total cost of the project into smaller elements whose costs can be estimated more easily. These costs can be broken down by the significant components of a project, the time when they occur in the project life cycle, and the category of resource cost they fall under (e.g. labour, materials, energy, etc.).

Consider the construction of a new highway. The costs for this project could be broken down into several major components, such as the design process, surveying the route, constructing the embankment, completing the road surface, and long-term maintenance costs (e.g. crack filling and snow removal). Each of these phases could be broken down into smaller cost components. For example, the construction of the road embankment would entail labour costs for labourers and geotechnical staff, material costs for the soil used as well as transportation costs to bring it to the work site, and equipment and fuel costs for operating the necessary construction vehicles. Each of these costs would be attached to a certain time period in the project life cycle. The provincial or federal government constructing the highway must look at the long term cost of maintaining the highway, which will influence the design process, construction process, and material choice. For example, a certain type of pavement might be more expensive, but would require lower maintenance costs over the road’s life cycle.

Once the costs of a project have been broken down to a suitable level of detail, they can be estimated using known cost data. In the early stages of a project, it can be difficult to gather detailed data on the expected costs associated with the project. However, with a common and well-known project type like a highway, the investor could estimate the costs with a fair degree of certainty based on the construction costs of many similar roadways. If the project were a new technology with no similar projects to compare it to, it would need to be estimated roughly using unit cost parameters, such as the expected cost per unit of construction or the cost per labour hour. If life cycle costing is continued throughout the project life, future costs can be estimated based on the costs incurred up to that point, allowing the LCC to be more accurate.

When estimating the life cycle costs for a project, there are three analysis methods to consider:

- engineering cost method,

- the analogous cost method, and

- the parametric cost method.

6.2.1 Engineering Cost Method

The engineering cost method is the most detailed of the three options, and is the preferred method whenever we have access to granular data about the operations and costs of a project. To estimate the entire cost of the project using this method, we treat the LCC as the sum of many components whose costs can be found individually. Each of these component costs is estimated using well established engineering and manufacturing standards, which are expected to be reasonably precise.

This method might be used, for example, in the construction of a new elementary school. The shape of the school, the number and size of the classrooms, and the dimensions of the gymnasium or school library are likely to be different from any other existing school. However, the basic construction materials (concrete, steel beams, metal roof decking) and their associated labour costs can be estimated by an experienced engineering firm after the design for the building has been decided.

6.2.2 Analogous Cost Method

The analogous cost method is less detailed than the engineering cost method, and draws more directly on historical data from analogous projects of a similar type, size, or operational type. For a given project, its cost would be estimated using the costs of other, similar projects, adjusting for variables like size, project location, and inflation.

For example, this method could be used in the design of a steel warehouse building. The design of these buildings is very standardized, and using basic data from suppliers and contractors the lead engineer could estimate the cost of building based on its major dimensions. This method could also be used to estimate the cost of running a new distribution centre for a large shipping company; if they already operate several similar centres, they could estimate the operational cost of a new facility based on its relative size and expected workload.

Note that this method depends heavily on the existence of a similar project with analogous costs. It cannot be applied to novel projects; for example it could not be applied to the CN Tower, the Panama Canal, or the International Space Station.

6.2.3 Parametric Cost Method

The parametric cost method relies on using historical data from certain project components, and scaling that data to the proposed project. This is similar to the analogous method, but This could be accomplished by developing a mathematical regression or progression formula representing the cost estimate.

This method could be used on a project to construct a new provincial highway. The transportation engineers working for the province could use existing data on the cost of roadway construction per kilometre, and then scale that cost by the length of the proposed new highway.

6.2.4 Life Cycle Costing Process

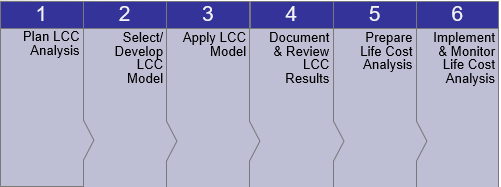

Life cycle costing is an ongoing process of analysis throughout the life of a project. When implementing it in a project, we can consider it a 6-step process, which we will discuss in detail here.

1. Plan Analysis

To analyze life cycle costs effectively, the method of analysis must be carefully considered in advance. A well-planned LCC analysis should consider the purpose and scope of the analysis, as well as its underlying assumptions, limitations, alternatives, required resources, and reporting schedule.

2. Select / Develop LCC Model

A LCC analysis should follow a well-defined model, and not every project is best analyzed by the same methods. For example, the LCC model for evaluating an industrial manufacturing operation with a few large, consistent costs and dependable profits will look much different from the model for a consulting firm which will have many different and fluctuating cash flows. An effective LCC model should break down costs efficiently, identify and omit redundant cost elements, source relevant data, use a reasonable estimation method, identify the uncertainty of estimates, integrate all costs, and document all assumptions.

3. Apply LCC Model

The crucial step of this process is applying the chosen LCC model to evaluate the project. Using the assumptions and processes previously selected, the LCC model should obtain data, develop cost estimates, validate results using historic data, identify significant costs, conduct sensitivity analysis, and quantify the differences between multiple alternatives.

4. Document and Review Results

After the basic processes of LCC analysis are complete, the results must be considered in order to draw meaningful conclusions, and make useful recommendations to the decision makers on the project. All results should be well documented, and should be reviewed critically and thoroughly so that the outcomes, implications, limitations, and uncertainties of the process are clear; the more detailed and well documented this review process is, the more useful it will be to any future or outside party which wishes to learn from your results. It may be fitting to subject the analysis to a formal review, to confirm that its assumptions, scope, model and recommendations of the LCC analysis are acceptable.

5. Prepare Life Cost Analysis (LCA)

Once the LCC analysis has been completed and reviewed, its results can be used to prepare a Life Cost Analysis (LCA) for the project. The LCA is a tool used to control ongoing costs for the project, and is similar to the LCC model, except that it substitutes estimated costs with the actual, ongoing costs of the project. The LCA works in real time to track project costs based on the targets set by the LCC, and may be updated if new data emerges. Using an LCA for a project could be considered analogous to using a flexible budgeting approach as discussed in Chapter 1 since both depend on making cost estimates and then tracking actual project costs based on those estimates.

6. Implement and Monitor LCA

Since the LCA is an ongoing process, after its creation and implementation it needs to be continuously monitored over the life of the project. The actual performance of a project, as determined by the environmental factors that influence project costs, needs to be closely watched in order to identify potential cost savings and avoid future risk for the project.